As the individual marketplace health insurance exchanges enter their 4th year of operation, growing pains still abound. Insurance providers are still struggling to determine appropriate pricing for various plans and are requesting a wide range of pricing changes – including some substantial premium increases – from state insurance regulators. The following are 5 key points regarding the upcoming open enrollment period for 2016:

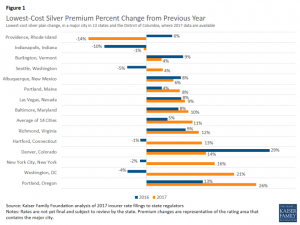

- Pricing changes vary widely and are fluctuating. A recently published Kaiser Family Foundation (KFF) Issue Brief highlights the substantial variation in premium pricing changes across markets – ranging from a drop of 14% to an increase of 26% for the lowest-cost silver plans. Further, insurers are struggling to determine a consistent price year after year.

Kaiser Family Foundation. Analysis of 2017 Premium Changes and Insurer Participation in the Affordable Care Act’s Health Insurance Marketplaces (2016).

For example, in Providence, Rhode Island, the lowest cost silver plan requested a 6% increase in 2016 and a 14% decrease in 2017. In Washington, D.C., the lowest cost silver plan requested a 4% decrease in 2016 and a 21% increase in 2017. Within individual state markets there is also tremendous variation between urban and rural plan pricing and availability, as some insurers only provide plans in certain locals within a state.

Kaiser Family Foundation. Analysis of 2017 Premium Changes and Insurer Participation in the Affordable Care Act’s Health Insurance Marketplaces (2016).

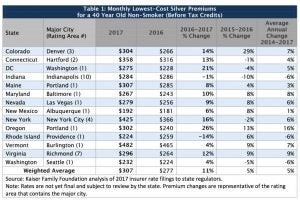

- Most premium increases will be offset with subsidies. Subsidies remain a critical piece of the individual health insurance marketplace – as approximately 80% of enrollees receive some form of subsidy. As the KFF Issue Brief notes, subsidies are tied to the premiums for the second-lowest silver plan, therefore enrollees may be protected from premium increases if they continue to enroll in lower cost plans. However, one challenge is that the lowest priced plans may differ from year to year. The KFF Issue Brief found that out of 14 states reviewed, 8 states had the same insurer offering the lower cost plans, while in 6 states the insurers with the lower cost plans were not necessarily the same year after year.

Kaiser Family Foundation. Analysis of 2017 Premium Changes and Insurer Participation in the Affordable Care Act’s Health Insurance Marketplaces (2016).

- Willingness to shop around. In order to minimize the impact of premium increases consumers must be willing to shop around for the best deal. This willingness to shop around has tradeoffs for both the insurer and the insured. The ability and willingness to shop around poses challenges for insurers in determining the premium prices on an annual basis, especially if a significant percentage of enrollees are willing to switch plans on an annual basis. Insurers must determine ways to ensure consumer loyalty beyond just offering the lowest price plan. Consumers also have to understand the tradeoffs with switching plans, which can include having to shifting to different providers and places of care. If a consumer knows they will need consistent care, they may be less willing to switch plans that would require transferring care to another provider. This may pose a financial challenge to such consumer if their plan’s premiums are projected to substantially increase.

- Young Invicibles. CMS recently issued a Fact Sheet highlighting its increased efforts and strategy to target enrolling young adults, often known as “young invincibles.” Young adults are still more likely than average to remain uninsured. Young adults are crucial for sustaining the health insurance marketplace as their relative good health helps subsidize the care for other individuals in poorer health who are guaranteed coverage regardless of their pre-existing conditions. Targeted efforts for the upcoming open enrollment period include: A) outreach to people who paid the individual responsibility penalty (about 45% of individuals paying the penalty or claiming an exemption were under 35); B) smarter outreach during Open Enrollment, especially towards the end of Open Enrollment; C) facilitating young adults’ coverage transition from family plans to individual plans; and D) utilizing public-private partnerships to engage young adults, including with Lyft, the American Hospital Association, and youth oriented public relations campaigns.

- Continuing Uncertainty. Factors external to individual health status and enrollment continue to cause uncertainty in the individual marketplace. Providers and insurers are pursuing aggressive consolidation strategies, which independently affect reimbursement rates and insurance prices. Ongoing regulatory activity and litigation, at both the state and federal level, continue to create an environment of uncertainty for the marketplace. Further, the upcoming election contributes to the environment of uncertainty. Regardless of which party prevails in the various elections, insurers must prepare for legislative and regulatory changes to the Affordable Care Act and the marketplaces operations.

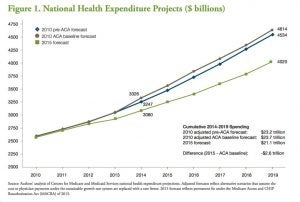

Reviewed from multiple angles, evidence demonstrates that the Affordable Care Act is accomplishing its goal of providing individuals with greater access to health insurance and ultimately health care. Further, projections demonstrate that the Act is further contributing to the “bending of the cost curve” with recent reports demonstrating a potential projected savings of approximately $2.6 trillion USD.

Robert Wood Johnson Foundation & Urban Institute. The Widespread Slowdown in Health Spending Growth Implications for Future Spending Projections and the Cost of the Affordable Care Act: An Update (2016)

Much remains to be resolved, however, and the need for certainty in the insurance market remains. Insurers, consumer groups, and both state and federal regulators must continue to work in a coordinated fashion to attempt to provide greater certainty to the individual marketplace with less extreme fluctuations in annual premium prices.