For a provision that dominated the health insurance reform debate for the past decade, the Affordable Care Act’s (ACA) individual mandate barely made headlines when the 2017 Tax Cuts and Jobs Act ended the tax penalty for uninsured individuals. It was an untimely end that everyone saw coming as the mandate’s popularity did not recover with the rest of the bill during repeal attempts. Criticism of the mandate was especially potent given the mandate’s importance to the overall health insurance reform effort—a centrality that conservative groups now contend should result in the ACA’s complete dismantling, The repeal of the individual mandate deserves more attention. What is happening to the health insurance marketplace in its absence, and what have both sides of the aisle proposed to replace it?

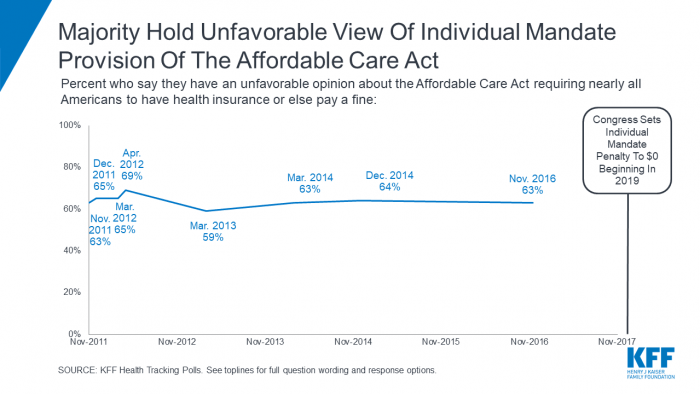

The Kaiser Family Foundation has consistently found a majority of Americans hold a negative view of the individual mandate.

The individual mandate was fundamental to the ACA because it made one of the law’s most popular provision—coverage of preexisting conditions—economically feasible in an industry characterized by market failures. The penalty would minimize the potential for a death spiral in insurance exchanges by encouraging healthy individuals to purchase insurance, effectively reducing premiums for sicker Americans. Subsidies would make health care affordable for younger, healthier individuals allowing them to avoid the mandate’s penalty. While still unclear how completely the ACA achieved these goals, the end of the mandate may be detrimental to the stability of health insurance exchanges.

If fewer healthy individuals purchase insurance, premiums will rise, pricing others out of the market. A 2017 Congressional Budget Office estimate showed that repeal of the individual mandate could lead to 13 million fewer insured and 10% higher premiums over the course of 10 years. In an analysis done since the repeal of the mandate’s penalty, the Kaiser Family Foundation suggested that the end of the individual mandate combined with looser regulated plans has resulted in 6% higher premiums on average and prevented several regions from experiencing projected reductions in premiums. As of now, the effective repeal of the individual mandate appears to have made insurance less affordable throughout the country. As we get closer to 2020, policy proposals put forward by both sides of the aisle may offer potential replacements for this portion of the law’s (now wobbling) three-legged stool.

The Republicans’ 2017 American Health Care Act (AHCA), which includes a similarly intentioned provision, suggests they should have understood the effects of repealing the individual mandate. Authors of the AHCA recognized the popularity of protections for preexisting conditions and included a watered-down requirement in the AHCA. As such, policymakers had to again tackle the problem of increased adverse selection in the marketplace. Thus, enters the ACHA’s subtly-titled Sec. 2710a: Encouraging Continuous Health Insurance Coverage. The AHCA does not mandate health insurance coverage for all individuals. It instead penalizes those uninsured after the enrollment period by instituting a 30% premium surcharge if they want to buy in later. Essentially, the AHCA penalizes healthy, uninsured individuals who sign up for coverage only after they fall sick. The AHCA pushed back the timeline of the ACA’s individual mandate penalty while transferring the burden of collecting it to insurers.

In this way, the AHCA’s version of the individual mandate serves both as a disincentive for healthy individuals to stay uninsured while explicitly attempting to internalize the cost of adverse selection in the market. While never implemented, the AHCA suggests how a conservative alternative to the individual mandate would be structured to reduce adverse selection while resisting language that directly requires the purchase of insurance. This method still comes with tradeoffs—closer adherence to conservative principles comes at the cost of clarity of intent. As the AHCA demonstrates, Republicans understood the need to reduce adverse selection in the health insurance market.

The other side of the aisle seems to have moved on from the individual mandate as a point of contention. All 2020 Democrats seem to favor a requirement for universal coverage. For those in favor of a Medicare for All plan, the individual mandate is redundant as the government would oversee automatic enrollment into a government-run health care plan. Others plans, like Rep. Rosa DeLauro’s Medicare for America bill (supported by Beto O’Rourke), would also use auto-enrollment (this time only for uninsured individuals) and avoid the mandate as well. For supporters of a public option, there is near-universal agreement to revive the individual mandate. Even as the Democratic primary field embraces a wide range of proposals, some version of a compulsory health insurance requirement appears in all plans.

As health insurance reform remains a top issue among voters in 2020, there is hope that future policy proposals on both sides of the aisle will address the need to curb adverse selection in the health insurance marketplace.

Graph courtesy the Kaiser Family Foundation